There are few phrases in the home improvement industry more powerful—or more misunderstood—than “0% financing”. For many homeowners, hearing those words immediately shifts the conversation away from critical long-term factors like total project cost, engineering quality, contractor stability, and lifecycle value, focusing instead entirely on the lowest monthly payment.

While financing is a valuable tool that helps consumers access renewable energy infrastructure while preserving personal liquidity, it is critical to understand how these promotional structures actually operate in the market. Following the conclusion of the federal Greener Homes Loan program in October 2025, many solar providers began widely marketing new “0% financing” alternatives.

However, these private structures are fundamentally different from former government programs, and “0% financing” rarely equates to free financing.

The Role of Hidden Dealer FeeS

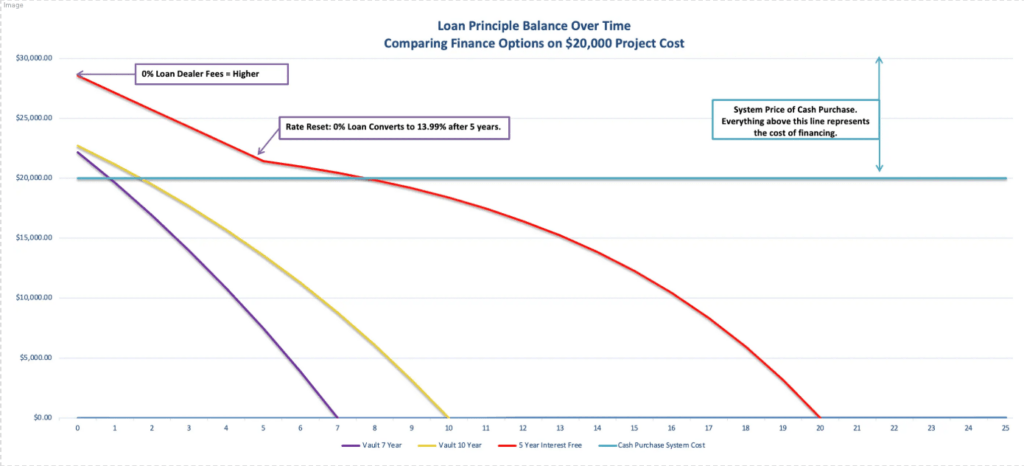

In many cases, third-party financing providers charge solar contractors significant upfront fees in exchange for offering promotional terms, extended amortizations, or low monthly payments. Commonly referred to as dealer fees, financing buy-downs, or merchant fees, these costs are typically recovered by embedding them directly into the upfront contract price.

The actual dealer fee associated with many of these new 0% loan products is approximately 29.99% added to the cash price of the solar system. In practice, this means the homeowner effectively finances the high cost of the borrowing itself from day one. Because these fees are wrapped directly into the principal, consumers are often presented with a final financed price without realizing that nearly one-third has been added to the original cost of the infrastructure just to access the “0%” headline rate.

Consequently, a crucial step for any homeowner evaluating a solar proposal is to explicitly ask the contractor for two separate figures:

- The Cash Purchase Price

- The Financed Project Price

Transparent contractors should comfortably disclose whether dealer fees exist, how financing impacts the baseline pricing, and what the total cumulative repayment looks like over the life of the agreement. If a company is unwilling or unable to clarify the difference between the cash and financed price, consumers should exercise extreme caution before proceeding.

Analyzing the Fine Print and Amortization Risks

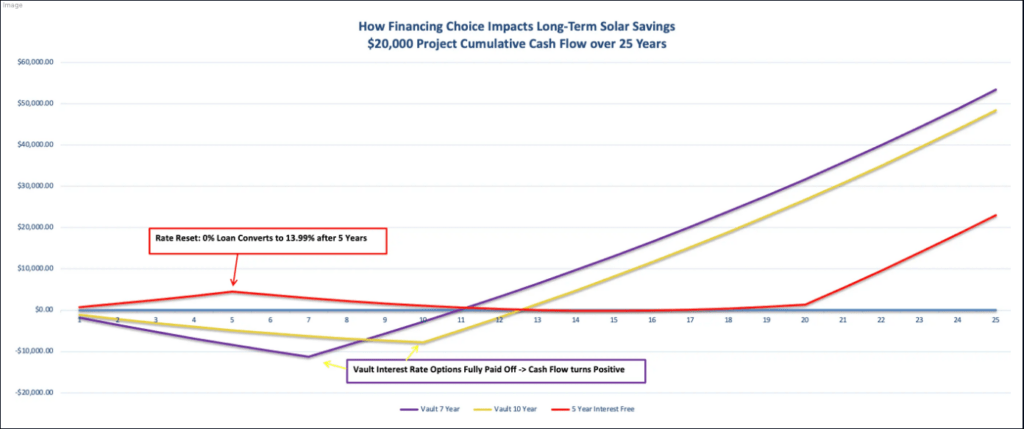

Promotional financing models are rarely as straightforward as their marketing headlines suggest. A common structure utilized in the current market involves a 5-year 0% promotional term amortized over a 20-year period. At the end of that initial 5-year window, any remaining principal balance automatically converts to a standard interest-bearing loan—often carrying high interest rates around 12.99%—for the remaining 15-year amortization.

To minimize consumer concern regarding this transition, sales representatives frequently advise clients to “simply roll the remaining balance into their mortgage at renewal”. However, this presents a significant financial risk:

- Refinancing vs. Renewal: In most cases, adding substantial debt to a home mortgage requires a full refinancing and qualification process, not a standard, automatic mortgage renewal.

- Lending Volatility: Refinancing is strictly subject to income verification, debt-to-income lending qualifications, credit approvals, and market interest rates at that future date.

- Changing Circumstances: Unexpected shifts in personal employment, macroeconomic lending regulations, or local housing market values could leave a homeowner physically unable to refinance after year 5, leaving them trapped in a high-interest loan structure.

Furthermore, some financing models assume that homeowners will receive independent grants or rebates and apply those lump-sum proceeds directly against the loan balance within the first few years. If those external funds are not applied, the monthly payments or overall amortization structures can change drastically.

Impact on Principal Repayment and Flexibility

Beyond interest rates, dealer fees fundamentally alter how principal repayment works. In a conventional fixed-term interest loan, interest accrues transparently over time rather than being locked into the principal upfront. This structure grants the homeowner flexibility, as any additional or early payments directly reduce the remaining principal balance and lower future interest costs.

Conversely, with many dealer-fee-based 0% loans, there is virtually no financial benefit to paying the loan off early. Because the 29.99% financing fee was already permanently baked into the principal on day one, the remaining principal balance after five years of consistent payments can still easily exceed the original cash price of the solar installation itself.

Conclusion: Evaluating Solar as Long-Term Infrastructure

A solar array is not a temporary or purely transactional consumer purchase; it is a decades-long infrastructure investment attached to a primary financial asset. Every project requires complex site engineering, electrical infrastructure constraints, utility interconnection approvals, and multi-decade production modeling.

The danger arises when financing becomes the primary product being sold, and the solar system itself becomes secondary. This shift prioritizes speed and transactional urgency over consumer education and long-term asset performance.

This information is not compiled to discourage consumers from financing their transition to renewable energy. Rather, it is designed to provide the clarity and transparency required to make an informed economic choice. In many cases, utilizing a conventional fixed-term bank loan, a home equity line of credit (HELOC), or another transparent lending product will provide significantly greater flexibility and lower long-term cumulative costs than a dealer-fee-based 0% financing program. Homeowners must carefully scrutinize total repayment costs, future remaining balances, and underlying refinancing assumptions before signing an agreement.

Want a transparent second opinion on your solar numbers?

Financing shouldn’t be a black box. If you’ve been offered a 0% deal and want to make sure there aren’t hidden fees baked into your contract principal, our Calgary team is here to help.